Car insurance prices in the UK are finally starting to fall in 2026. After a sharp spike over the past couple of years, the market appears to be easing.

But here’s the problem…many drivers are still seeing higher renewal quotes.

So what’s actually going on?

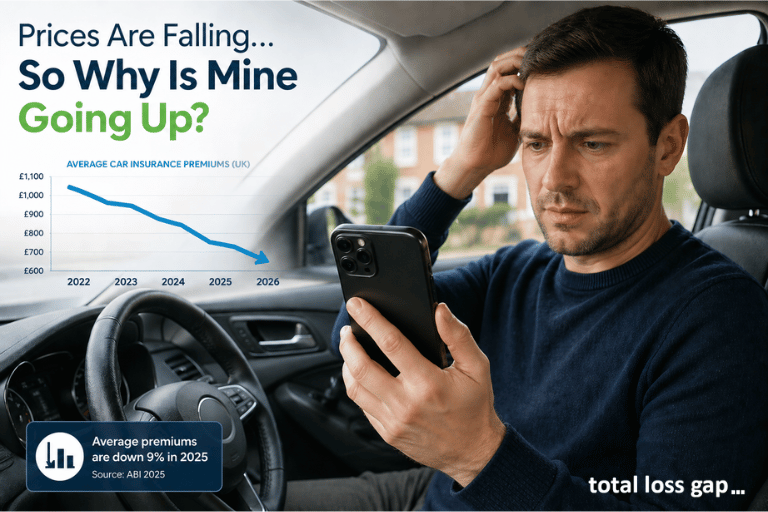

Car insurance prices are falling… on paper.

Recent data shows a clear downward trend in average premiums.

According to the Association of British Insurers (ABI), the average annual comprehensive motor premium fell by around 9% year-on-year, sitting at approximately £564 in 2025. That is a significant drop considering all of the other ‘cost-of-living’ increases currently seen in the UK.

Other industry trackers, including pricing data from WTW, show early 2026 averages closer to £700.

Overall, prices are coming down.

But that doesn’t mean all drivers are necessarily paying less.

Why premiums are easing

The recent drop is largely a correction after a period of sharp increases.

Between 2022 and 2024, UK motor insurance premiums increased for several reasons.

- Rising repair costs - inc

- Supply chain disruption

- Increased labour costs

- Higher vehicle values post Covid

It was reported that premiums were averaging around £1,000 during that period, so whilst it is a significant drop in recent times, cost pressures on insurers remain high.

However, inflation has come down and stabilised somewhat, and supply chain issues have improved. These are all factors that have helped lower insurers' costs.

Motor Insurance is one of the largest consumer insurance markets. The market is very competitive in 2026, which is the biggest driver of the premium drops. How long that may continue is another matter.

So why are some drivers still paying more?

Despite falling average renewal quotes, many motorists are still seeing higher renewal quotes.

Prices are still historically high

Even after recent reductions, premiums remain well above pre-2022 levels.

While prices are falling year-on-year, many drivers are still paying more than they did a few years ago.

Repair and claims costs are still rising

Behind the scenes, claim costs are still increasing. There has been a recent trend of

repair costs rising year-on-year, driven by the cost of advanced tech like cameras and airbags, as well as longer repair times.

Falling premiums don’t mean falling costs - insurers are still under pressure.

Pressure on insurers to raise premiums again

However, we may have seen prices at or approaching the bottom. If upward costs keep rising, then annual premiums may well start to rise again.

Your personal risk matters more than averages

Headline averages don’t reflect individual pricing.

Factors like postcode still play a major role. For example, drivers in London typically pay more than the UK average. The cheapest place for car insurance is Wales, according to Which?, who report premiums in the principality are up to 84% cheaper than those in the capital.

The hidden shift: drivers taking on more risk

To keep premiums affordable, many drivers are:

- Increasing voluntary excess

- Reducing optional cover - legal expenses, windscreen cover, roadside recovery, etc

- Choosing cheaper policies

This lowers the upfront cost, but increases exposure later.

We showed

how we saved 27% on our motor insurance premium by opting for a higher excess contribution. However, by taking a higher excess, you face a higher bill if you do make a claim on your insurance. Taking a motor excess insurance policy can help mitigate this risk.

The cost hasn’t gone - you just take more risk on yourself.

What happens if your car is written off?

If your car is written off, your insurer typically pays its market value at the time of the claim.

A vehicle can be written off if it is involved in an accident, is stolen, is in a fire, or is in a flood. Your motor insurer decides that the vehicle is beyond economic repair. They

write the vehicle off as a total loss and may only pay out the current market value to you in settlement.

This can lead to a significant shortfall.

Example:

- Paid £25,000

- Insurer pays £17,000

- £8,000 loss due to depreciation

Why this matters more in 2026

Several trends are increasing financial risk:

- Higher vehicle prices

- Larger excesses

- More cost-conscious policies

All of these increase the likelihood of a shortfall after a total loss.

Where GAP Insurance fits in

GAP Insurance covers the difference between your insurer’s payout and either:

- The price you originally paid

- Or the cost of replacing your vehicle

Or you can get a quote directly here:

What UK drivers should do now

The single message must always be do not accept your renewal premium without shopping around. Price comparison websites are great for providing you with a clear comparison of multiple insurers. Remember, not all insurers will appear on these facilities, so it is important to check elsewhere too.

Comparison websites won’t work for everyone, but they are a great way to benchmark.

The bottom line

Car insurance prices may be falling in 2026, but that doesn’t mean the risks have gone away.

The old advice is still the best: shop around, do not blindly accept renewal premiums, and only take the additional cover you really need. Stick to this, and you will still get the best value.