What Is the Best Type of GAP Insurance for Me?

The

best type of GAP Insurance depends on how you bought your car, how old it is and what level of protection you want if the vehicle is written off or stolen.

In general, Vehicle Replacement GAP Insurance is often seen as the highest level of protection for newer vehicles because it can cover the cost of replacing your car with a new equivalent model if prices rise after purchase.

However, that does not automatically mean it is the best option for everyone.

For some drivers, Return to Invoice GAP Insurance may offer a better balance between protection and cost. Others may benefit more from a combined GAP Insurance policy that protects against finance shortfalls and depreciation.

The right policy depends on:

- whether the vehicle is new or used

- how the vehicle was financed

- the age and mileage of the vehicle

- how long you plan to keep it

Which GAP Insurance Is Usually Best?

As a rough guide:

- Discounted cars, as often happens with brand-new cars, are often best suited to Vehicle Replacement GAP Insurance

- Used cars are commonly covered with Return to Invoice GAP Insurance

- PCP and hire purchase agreements can benefit from combined GAP Insurance features

- Lease vehicles usually require Contract Hire or Lease GAP Insurance

- Older vehicles may need specialist GAP Insurance policies with extended age and mileage limits

That said, different insurers use different underwriting rules and product structures, so there is no single policy that is automatically best for every driver and every situation.

Is Vehicle Replacement GAP Insurance the Best?

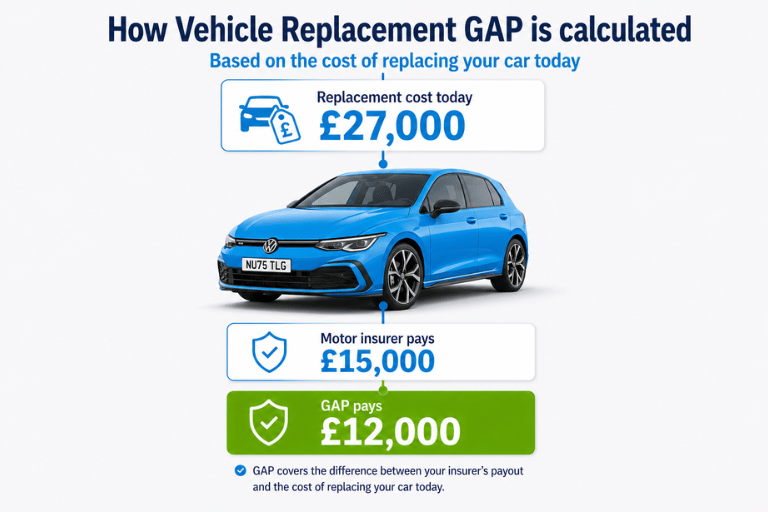

Vehicle Replacement GAP Insurance (sometimes called VRI GAP Insurance) is designed to cover the difference between your motor insurer’s payout and the cost of replacing your vehicle with an equivalent model at the time of claim.

This can become important if vehicle prices increase after you buy the car.

For example, if you paid £25,000 for a new vehicle but the same new model now costs £27,000 to replace, Vehicle Replacement GAP Insurance may help bridge that larger replacement gap.

This is one reason why many people view Vehicle Replacement GAP as the highest level of protection offered for eligible vehicles.

It can work particularly well for:

- brand-new cars

- electric vehicles

- heavily discounted vehicle purchases

- cars are likely to increase in replacement cost over time

However, Vehicle Replacement GAP Insurance is not always available on older vehicles, and it can cost more than Return to Invoice GAP Insurance.

There is no guarantee that VRI will provide a better settlement than an RTI GAP policy, particularly on older vehicle buys.

You may also want to read:

The Total Loss GAP Vehicle Replacement GAP advantage

Be warned - not all GAP Insurance products bearing the Vehicle Replacement GAP name work the same way. Assuming so could cost you thousands in a claim.

Total Loss GAP provides a 3-in-1 solution with VRI cover. Find out why this is better than nearly all other VRI GAP products on offer in the UK today.

Is Return to Invoice GAP Insurance Better Value?

For many drivers, yes.

Return to Invoice (RTI) GAP Insurance is the most common form of cover because it is often available on both new and used vehicles and can provide very strong protection at a lower premium than Vehicle Replacement GAP Insurance.

RTI GAP cover is often the type offered at motor dealers, who often ignore the potentially more complex, but also more comprehensive, VRI GAP Insurance options.

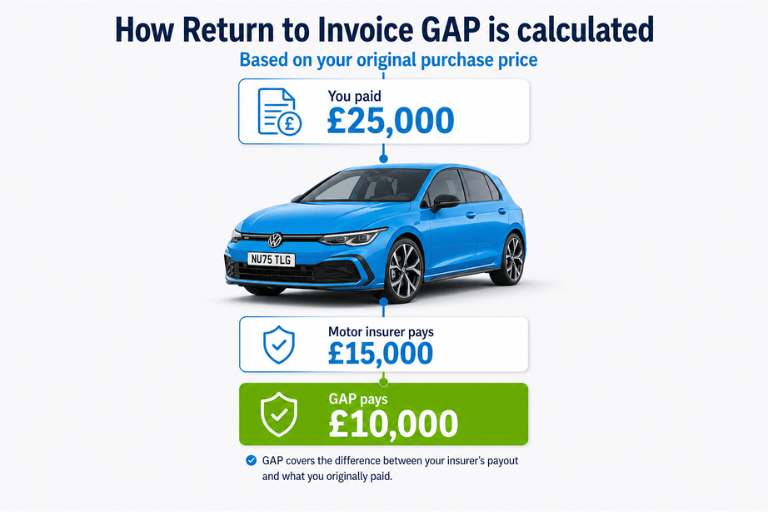

Rather than covering the cost of an equivalent replacement vehicle, RTI GAP Insurance is designed to bridge the gap between your motor insurer’s settlement and the original invoice price you paid for the car.

For many vehicles, especially used cars, this can still represent a perfectly adequate level of protection.

RTI GAP Insurance is commonly chosen for:

- used vehicles bought from dealers

- new and nearly new cars

- financed vehicles

- customers wanting strong protection without paying for full replacement cover

What Is Best for PCP or Hire Purchase Finance?

If your vehicle is financed through PCP or hire purchase, the best option is often a combined GAP Insurance structure (either RTI or VRI GAP).

This is because the finance settlement, invoice price and replacement value can all differ depending on when a total loss occurs.

Some combined GAP Insurance policies can protect whichever figure is highest at the time of claim, whether that is:

- the remaining finance balance

- the original invoice price

- or the replacement vehicle cost

This can offer increased flexibility than basic Finance GAP policies.

Related guides:

What About Lease Cars?

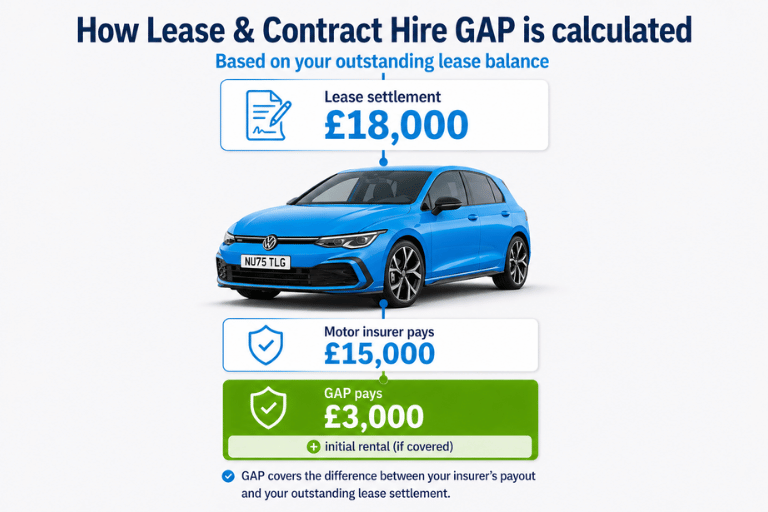

Lease and Contract Hire vehicles require a different type of GAP Insurance.

Because you do not own the vehicle, the main concerns are often the lease company’s early termination fees, lease-end charges, and any remaining rentals after a total loss.

You do not have the option to own the vehicle under a lease, so Return to Invoice or Vehicle Replacement-style cover is not needed.

This is why Lease GAP Insurance exists as a specialist product type.

You may also want to read:

Is GAP Insurance Worth It on Used or Older Cars?

Potentially, yes.

A common misconception is that GAP Insurance is only relevant for brand-new vehicles. In reality, some insurers also offer cover for older and higher-mileage cars, particularly where finance balances are a concern, or replacement costs are still relatively high.

This can be especially relevant for:

At Total Loss GAP, standard RTI policies are available for vehicles up to 8 years old and 80,000 miles at policy purchase, with some specialist insurer options extending to vehicles up to 10 years old and unlimited mileage.

What Should I Look for in the Best GAP Insurance Policy?

The “best” GAP Insurance policy is not always the cheapest.

It is important to compare:

- the type of GAP cover offered

- maximum claim limits

- vehicle age and mileage limits

- whether finance shortfalls are included

- excess contributions

- flexibility of the policy wording

The quality of the underwriter and the policy features can often matter far more than simply choosing the lowest premium.

You may also want to read:

The Bottom Line

Vehicle Replacement GAP Insurance is often considered the highest level of protection because it can cover rising replacement-vehicle costs after a total loss.

However, the best GAP Insurance for you depends on your circumstances.

For many used vehicles, Return to Invoice GAP Insurance may offer excellent value. For PCP or hire purchase agreements, combined GAP Insurance policies can provide additional flexibility when finance balances are higher than expected.

The most important thing is choosing a policy that suits:

- your vehicle

- your finance agreement

- your budget

- and the level of protection you actually want or need

Always check the policy wording, eligibility criteria and cover structure carefully before purchasing GAP Insurance.

Reviewed by

Mark Griffiths, Founding Director and GAP Insurance expert

Last reviewed: 11th May 2026

This quote was then compared against many online providers for alternative quotations.

This quote was then compared against many online providers for alternative quotations.