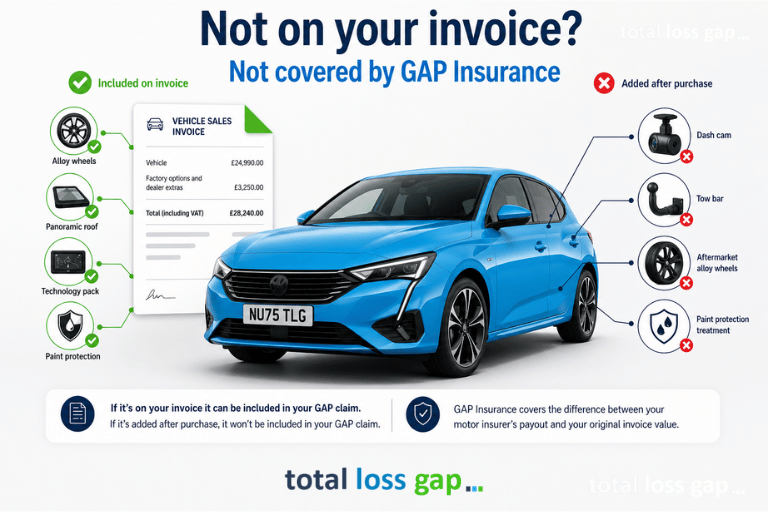

Does GAP Insurance Cover Accessories Fitted After Purchase?

GAP Insurance does not cover accessories fitted after purchase if they are not included on the vehicle’s original sales invoice.

These items will not invalidate your

GAP Insurance policy, as long as your motor insurer accepts them and they do not affect the insurer’s settlement value. However, no additional value for these accessories will be included in any GAP claim.

In short, if it’s not on the original invoice, it won’t be included in your GAP payout.

This is an important distinction that many drivers misunderstand.

What counts as “accessories fitted after purchase”?

Accessories fitted after purchase are any items added to your vehicle

after you have taken ownership that are

not listed on the original sales invoice.

Common examples include:

- Dash cams fitted weeks or months later

- Tow bars fitted after delivery

- Paint protection treatments that are applied after purchase

- Upgraded alloy wheels bought separately

- Audio or infotainment upgrades

Even if these items are professionally installed and add value to the vehicle, they are treated as separate purchases from the vehicle.

Why doesn’t GAP Insurance cover these accessories?

GAP Insurance works from a fixed starting point: your vehicle’s original invoice price.

At the time of a claim, the policy compares:

- What you originally paid for the vehicle

- What your motor insurer pays out (market value at the time of loss)

The difference between these figures is the “gap”.

Accessories added after purchase are not included on the original invoice, so they are excluded from

the GAP calculation. (see how GAP Insurance works in our

GAP Insurance 101 guide)

In simple terms:

If it wasn’t included in the vehicle purchase price, it won’t be included in the GAP settlement.

Do post-purchase accessories affect your GAP Insurance cover?

No, adding accessories after purchase does not cancel or invalidate your GAP Insurance.

Your policy will still work as intended if your vehicle is written off or stolen.

The only limitation is:

- These accessories won’t increase your GAP payout

- They won’t be factored into the shortfall calculation

- If the addition of these accessories impacts your motor insurance, by either invalidating cover or reducing the settlement, then your GAP Insurance claim may be impacted in the same way.

What about your motor insurance?

Whether your accessories are covered at all depends on your motor insurer, not your GAP policy.

If your motor insurer:

- Includes the accessories in their settlement → your GAP claim will go ahead as normal (but still won’t add extra value for them)

- Excludes the accessories → GAP Insurance will not cover them either

GAP Insurance does not act as a backup for items your motor insurer refuses to cover.

Real-world examples

Here’s how this typically works in practice:

- Dash cam fitted 2 months after purchase

→ Not included in GAP claim

- Tow bar added after delivery

→ Not included in GAP claim

- Paint protection that is applied after purchase

→ Not included in GAP claim

- Factory-fit options or dealer extras on the original invoice

→ Usually included (see our guide to factory-fit options and dealer extras)

How to make sure your extras are covered

If you want accessories to be included within your GAP cover, the safest approach is:

- Arrange for them to be fitted before delivery

- Ensure they are listed on the vehicle sales invoice

- Keep full documentation as proof of purchase

If they appear on the invoice, they can form part of the insured value used in a GAP claim.

How does this fit into your overall GAP cover?

GAP Insurance is designed to protect the difference between your motor insurer’s payout and your original vehicle value.

That value is based on what you paid at the point of purchase, which is why your invoice detail is so important.

If you’re unsure how different policies calculate this, it’s worth understanding the differences between Return to Invoice and Vehicle Replacement cover, as this can affect how your claim is settled.

You can also see how this fits into the bigger picture in our GAP Insurance 101 guide, which explains how cover works in more detail.

Key takeaway

If an accessory is not listed on your original vehicle invoice, it will not be included in a GAP Insurance claim, even if it was added later. If you’re planning to add extras to your vehicle, it’s worth checking how your GAP policy treats them before you buy.

Related GAP Insurance guides

Thinking about GAP Insurance?

If you’re considering GAP Insurance, it’s worth checking how your policy treats vehicle value and extras before you buy.

You can also

get a quick quote to see your cover options and pricing based on your vehicle.

Reviewed by

Mark Griffiths, Founding Director and Insurance expert

Last reviewed: 28th April 2026