Call Monday-Friday 9am - 6pm Closed Weekends & Bank Holidays

[ Contact Us ]

Need Help? Calling from a mobile please call 0151 647 7556

0800 195 4926Do you have a question? or need help?

Call Monday-Friday 9am - 6pm Closed Weekends & Bank Holidays,

GAP Insurance (Guaranteed Asset Protection) covers the difference between your motor insurer’s payout and what you originally paid, still owe on finance or lease, or need to replace your vehicle if it’s written off or stolen.

Get a GAP Insurance quote in minutes and compare cover options with flexible payment plans available.

Buy GAP Insurance from an experienced UK provider using only secure, ‘A’ rated insurers. Total Loss GAP is one of the best-known independent providers, trusted by UK vehicle owners for over a decade.

GAP Insurance from £77.89. Pay in full, over 6 months at 0%, or from £2.58 per month on longer plans up to 48 months.

Options include Return to Invoice, Vehicle Replacement and Lease & Contract Hire GAP Insurance, for vehicles valued from £5,000 to £150,000.

Providing GAP Insurance since 2010. FCA authorised, FSCS protected, Member of BIBA.

Not available on comparison websites.

GAP Insurance helps cover the financial shortfall if your car is written off or stolen and your motor insurer pays less than the amount you originally paid, owe on finance, or need to replace the vehicle.

Because cars can depreciate quickly, many drivers face a significant financial shortfall after a total-loss claim.

At Total Loss GAP, we offer a range of cover options from A-rated insurers, including:

• Return to Invoice GAP

• Vehicle Replacement GAP

• Lease & Contract Hire GAP

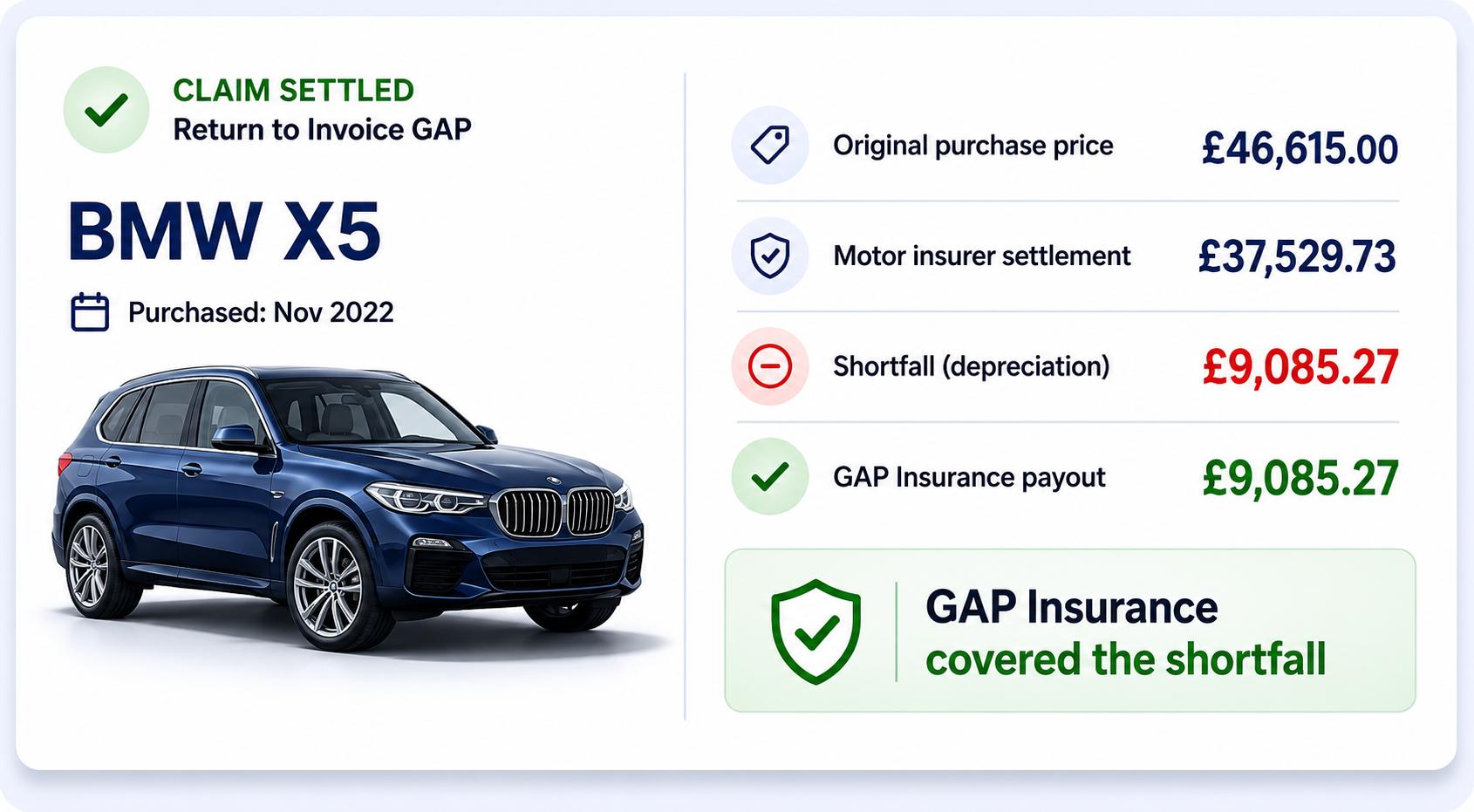

The real-life claim example opposite shows how GAP Insurance can help cover the difference between your motor insurer settlement and the original vehicle value, as Return to Invoice GAP would.

Vehicle Replacement GAP Insurance helps protect you if your vehicle is written off or stolen and your motor insurer’s settlement is no longer enough to replace it with an equivalent vehicle.

As the most comprehensive cover, Vehicle Replacement GAP can help cover the higher of:

• the original invoice price you paid for the vehicle

• the cost of replacing the vehicle like-for-like at the time of claim

• the outstanding finance settlement

This can be particularly valuable if vehicle prices have increased since you bought the car.

• Brand-new vehicles

• Electric and hybrid cars

• PCP and HP finance agreements

• Drivers wanting the highest level of GAP protection

• Protection against rising vehicle replacement costs

• Covers significant depreciation shortfalls

• Helps replace your vehicle with an equivalent model

• Often considered the most comprehensive type of GAP Insurance

Return to Invoice GAP Insurance helps cover the difference between your motor insurer’s payout and the original invoice price you paid for your vehicle if it is written off or stolen.

As the most popular type of cover, RTI GAP Insurance can help top up your motor insurance settlement if the car is written off or stolen.

The policy can usually cover the higher of:

• the original invoice price you paid

• the outstanding finance settlement

This means you could clear any remaining finance and recover the original value of your vehicle purchase.

• New and nearly-new vehicles

• PCP and HP finance agreements

• Drivers wanting strong protection at a lower premium than Vehicle Replacement GAP

• Customers concerned about vehicle depreciation

• Helps protect your original vehicle investment for cash buys

• Covers depreciation shortfalls after a total loss

• Can clear outstanding finance balances

• One of the most popular types of GAP Insurance in the UK

Lease & Contract Hire GAP Insurance is designed specifically for leased vehicles where you do not own the car.

If your leased or contract hire vehicle is written off or stolen, your motor insurer’s payout may not cover the remaining lease balance or early termination charges owed to the finance company.

Lease GAP Insurance can help cover:

• outstanding lease rentals

• early termination charges

• financial shortfalls following a total loss

• initial rental protection on selected policies

This helps reduce the risk of being left with a large financial liability after a write-off claim.

• Personal lease vehicles

• Business contract hire agreements

• Drivers who do not own the vehicle outright

• Designed specifically for lease and contract hire agreements

• Helps cover early termination charges

• Can protect outstanding lease liabilities like outstanding rentals

• Available for cars, EVs and light commercial vehicles

5 Star rated features and cover not found on comparison websites. No hidden fees, paid placements, ratings or third-party 'recommendations'.

Directly authorised and regulated by the FCA in the UK (FRN 821163) and covered by the FSCS, safe and protected.

Flexible cover, including deferred start dates (if you have 'new car replacement' cover).

UK-based customer service and claims support, real people when you need them.

Rated 'Exceptional' by Feefo with a customer service score of 4.9 out of 5 from over 6,000 verified customers.

Proven history, a 99% claims acceptance rate with an average claim settlement of £8,079.19 in 2025.

Featured and discussed on MoneySavingExpert, Which?, What Car?, TrustPilot, The Car Expert, Honest John, PistonHeads, Bimmerforums and Auto Express.

Additional reassurance from insurers with independently assessed strong financial ratings

No long lists of 'excluded' vehicles

Up to 4-year terms available

Experienced UK-based support teams

We are here to help!

Including 3 or 6 months at 0%

Or between 12 and 48 months on a funded agreement

If you have 'new car replacement' with your car insurance

Only pay for the GAP protection you actually need

Changing your vehicle?

One free policy transfer included

From October 2025, all new GAP Insurance policies from Total Loss GAP will be backed only by ‘A’ rated insurers.

Every GAP policy is a promise to pay if you need to claim. The strength of that promise depends on the insurer’s financial stability.

‘A’ rated insurers have been independently assessed by global credit agencies for their ability to meet claims, even in tough times. Unrated insurers haven’t, and are generally seen as higher risk and more likely to fail.

That’s why we now only work with 'A' rated insurers for our new Guaranteed Asset Protection (GAP) Insurance products. If you ever need to claim, you deserve the reassurance that your insurer will be there to pay, in full and without delay.

If you are comparing GAP Insurance providers, then checking the credit rating of their underwriter may be a good place to start.

Get a GAP Insurance quote from an 'A' rated Insurer from Total Loss GAP today.

Rated 4.9/5 from over 6,000 verified customer reviews

Eligible insurance policies benefit from FSCS protection

Proud members of BIBA for over a decade

5 Year Return to Invoice GAP

GAP Insurance settlement paid

£13,695

4 Year Vehicle Replacement GAP

GAP Insurance settlement paid

£19,392

5 Year Return to Invoice GAP

GAP Insurance settlement paid

£6,948

A GAP Insurance claim can begin once your motor insurer declares your vehicle a total loss following an accident, theft, fire or flood.

Your motor insurer must first settle your claim based on the market value of the vehicle. GAP Insurance can then help cover the remaining shortfall.

Yes, for many drivers, GAP Insurance can help protect against depreciation if your car is written off or stolen.

Cars can lose value quickly, particularly newer and electric vehicles, potentially leaving a shortfall between the insurer payout and what you originally paid

At Total Loss GAP, policies start from £77.89 for 2 years' cover, with options available between 2, 3 and up to 4 year terms.

The cost depends on the value of your vehicle, the type of GAP Insurance you select, and the length of cover you choose.

GAP Insurance won't cover if your motor insurer does not declare the vehicle a total loss, and pay out, or if exclusions apply.

Common exclusions include negative equity carried over from a previous finance agreement and extras not shown on the sales invoice.

Compare GAP Insurance cover, learn about the benefits of purchasing online, and explore answers to common questions about claims, cancellations and eligibility.

Our GAP Insurance knowledge hub provides guides and FAQs.

GAP Insurance is designed to protect you in situations where your motor insurer’s payout does not fully cover your financial position. This typically includes:

- Returning you to your original purchase price if your car has depreciated significantly

- Clearing an outstanding finance or lease balance if you owe more than the insurer pays

- Helping you replace your vehicle like-for-like rather than settling for a lower-value replacement

The exact cover depends on the type of GAP Insurance you choose, such as Return to Invoice, Vehicle Replacement or Contract Hire/Lease GAP.

For many drivers, yes. Cars lose value quickly, and if yours is written off or stolen, your motor insurer will usually pay only the current market value.

GAP Insurance can protect you from a significant financial shortfall, particularly if you have finance or a lease, or want to replace your vehicle like-for-like.

.png "GAP Insurance - Total Loss GAP")

.png "Get a GAP Insurance UK Quote from Total Loss GAP")

When a car is written off or stolen, your motor insurer typically pays only the current market value, not the amount you paid. With vehicles depreciating quickly, this can leave a large financial shortfall.

Here’s where GAP Insurance steps in:

Your motor insurer pays the market value.

Your GAP policy covers the shortfall - up to the original invoice price, your outstanding finance, or the cost of a replacement vehicle (depending on the policy). See how GAP Insurance claims are calculated

You’re not left out of pocket - you can clear finance or put the full amount towards a new car.

Example: You bought your car for £25,000. Two years later, it’s stolen, and your insurer values it at £16,000. GAP Insurance covers the missing £9,000, so you get back your original purchase price in full.

.png "Buy GAP Insurance online")

A brand-new car can lose between 15% and 35% in value in the first year alone.

A used car typically loses 10% to 15% of its value each year.

Motor claims hit a record £11.7 billion in 2024, with the average claim rising to £5,300.

Our average GAP Insurance claim since 2019 is £5,937.49.

In 2025, our average GAP Insurance payout rose to £8,079.19.

We have seen over £6.5 million paid out in GAP Insurance claims to our customers from January 2019 to March 2026.

Get an instant GAP Insurance quote online in less than 60 seconds, or call our friendly, award-winning team to learn more.

Compare GAP Insurance cover, learn how policies work, and explore the different types of protection available for financed, leased and privately owned vehicles.

If you want to explore specific topics in more detail, you can use the guides below.

View all GAP Insurance guides and FAQs

Ready to compare GAP Insurance cover? Get an online quote in under 60 seconds.

GAP Insurance is often more affordable than you might expect.

Prices start from £77.89 for 2 years, £98.97 for 3 years and £159.98 for 4 years.

Most policies range from £100 to £400, depending on your vehicle, its value, the cover level, and the policy term.

The average cost of each type of GAP Insurance, from November 2025 to April 2026, is:

Return to Invoice GAP - £231.55

Vehicle Replacement GAP - £290.07

Lease & Contract Hire GAP - £296.52

Most policies range from £100 to £400, depending on your vehicle, its value, the cover level, and the policy term.

Pay in full:

Visa

Mastercard

Amex

Apple Pay

Google Pay

PayPal

Pay Monthly:

PayPal Pay-in-3

0% over 6 months

Longer payment plans up to 48 months

Return to Invoice GAP, Vehicle Replacement GAP and Contract Hire & Lease GAP available, with flexible payment options.

GET MY QUOTETyre Insurance

Tyre Insurance covers repair or replacement costs following accidental or malicious tyre damage.

Tyre & Alloy Wheel Cover

Cover for tyre damage and alloy wheel repairs following accidental or cosmetic damage.

Alloy Wheel Cover

Cover for alloy wheel repairs following accidental or cosmetic wheel damage.

SMARTCare Cosmetic Cover

Cover for alloy wheel and minor bodywork cosmetic repairs following accidental damage.

Motor Excess Insurance

Recover your motor insurance excess costs following an at-fault or non-fault insurance claim.

Fair Value to customers and a fair deal to all our policyholders and website visitors.

Anyone selling Gap insurance must be regulated by the Financial Conduct Authority in some form or another. Fair Value Assessments are part of Consumer Duty and are an ongoing process of monitoring, maintaining, supervising, and ensuring that customer outcomes are front and centre in every organisation.

We have worked and will continue to work with our suppliers, underwriters, and the Financial Conduct Authority (FCA) to ensure that all our policies offer Fair Value and that you get a fair deal. This applies not only to gap insurance cover but to all policies we provide.

This ongoing work allows us to monitor, measure, and evaluate our policy performance and insurance premiums, from measuring claims rates to ensuring that our policies perform the way you expect them.

When would you not need a gap insurance policy?

We are a Gap Insurance Provider, so naturally, we think protecting yourself with a gap insurance policy is worthwhile .

We see first-hand the financial benefits when gap insurance policyholders' vehicles have been written off.

So when would you not need a gap insurance policy?

1. If you are fortunate enough to have enough savings or financial backing, you don't worry about paying off finance agreements or being able to top up any shortfall to buy another vehicle.

2. If you have bought a new vehicle, have a new one for old clause within the terms of your motor insurance policy and are happy with any terms they have.

.png "Buy GAP Insurance online")